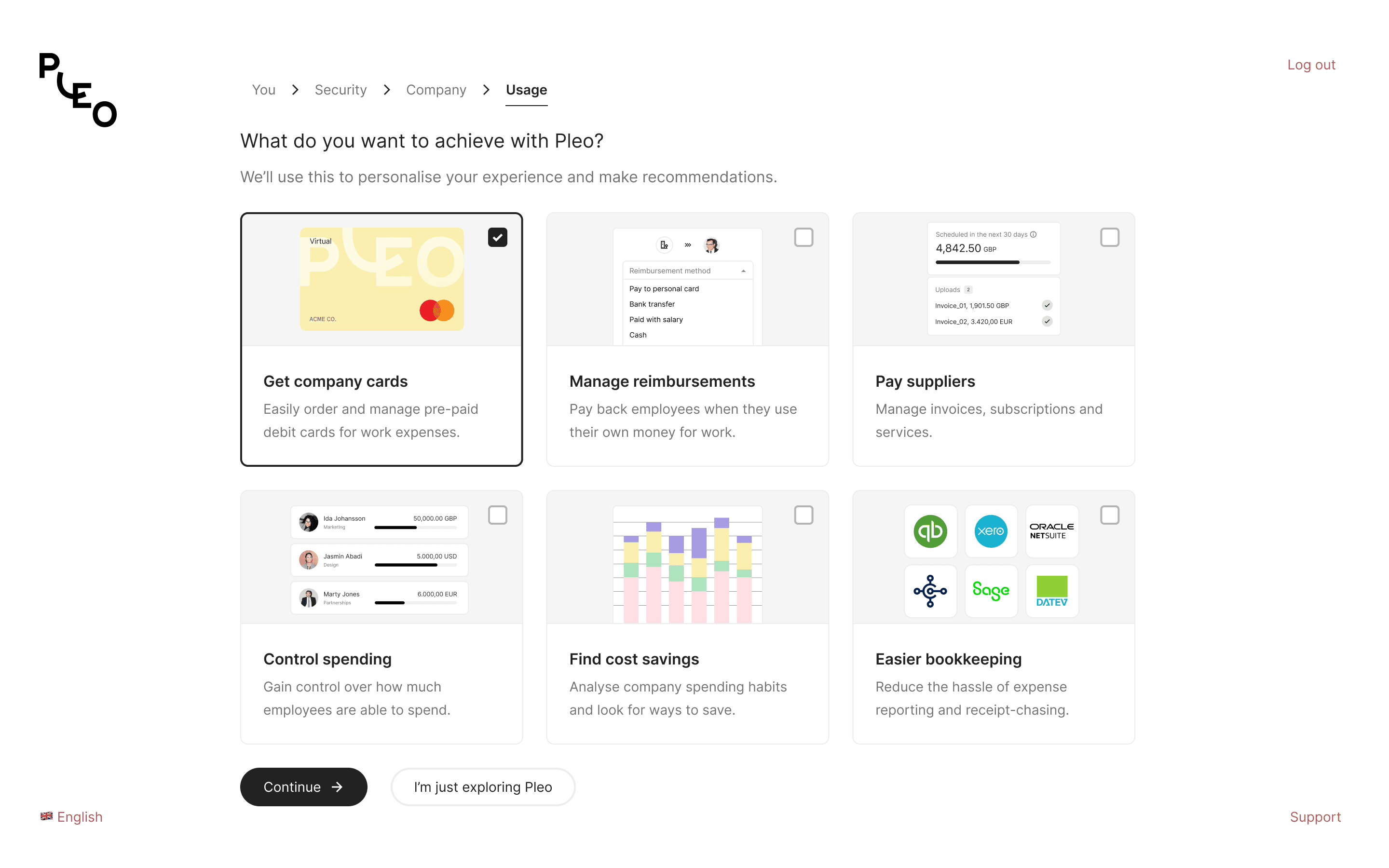

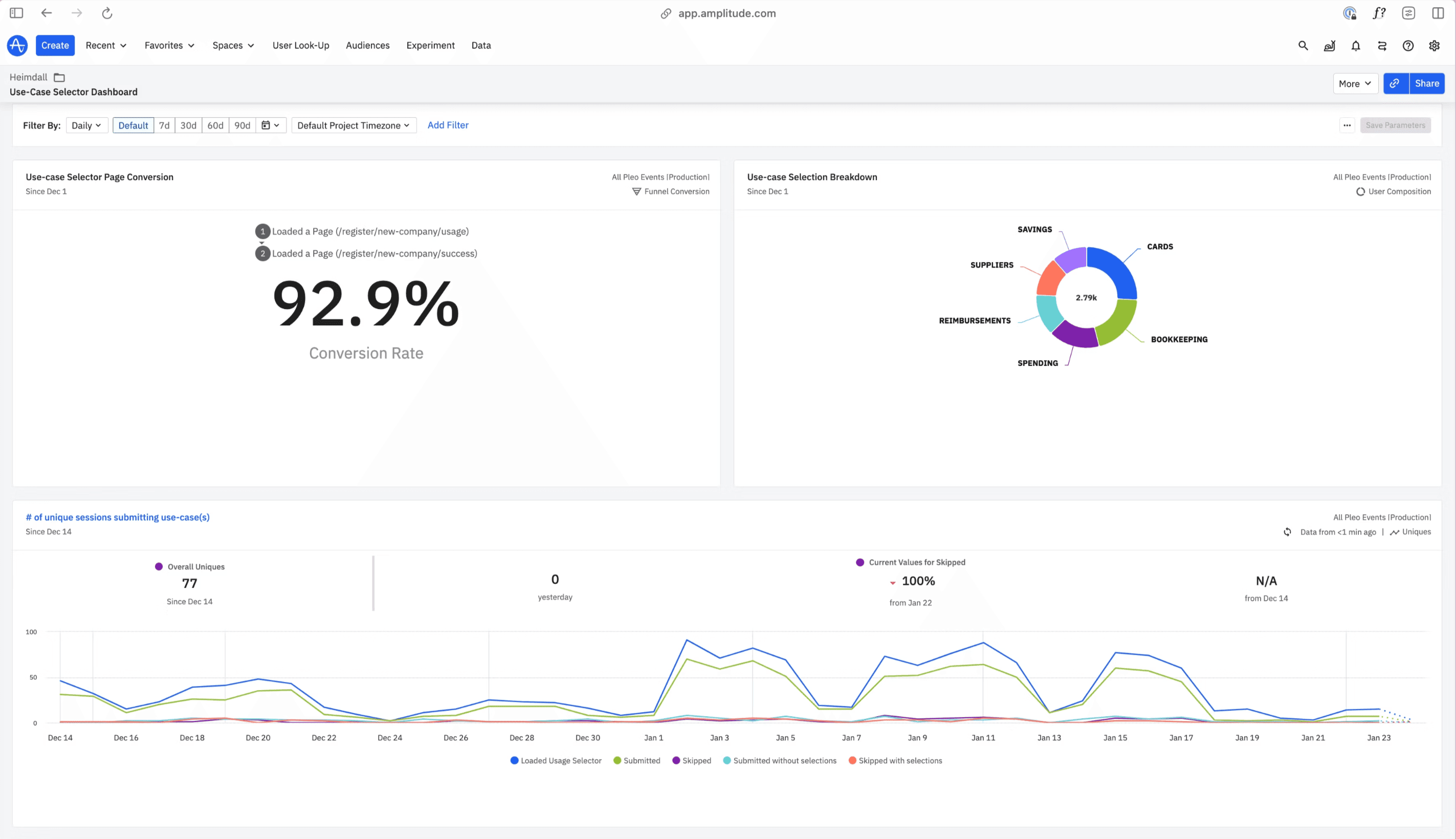

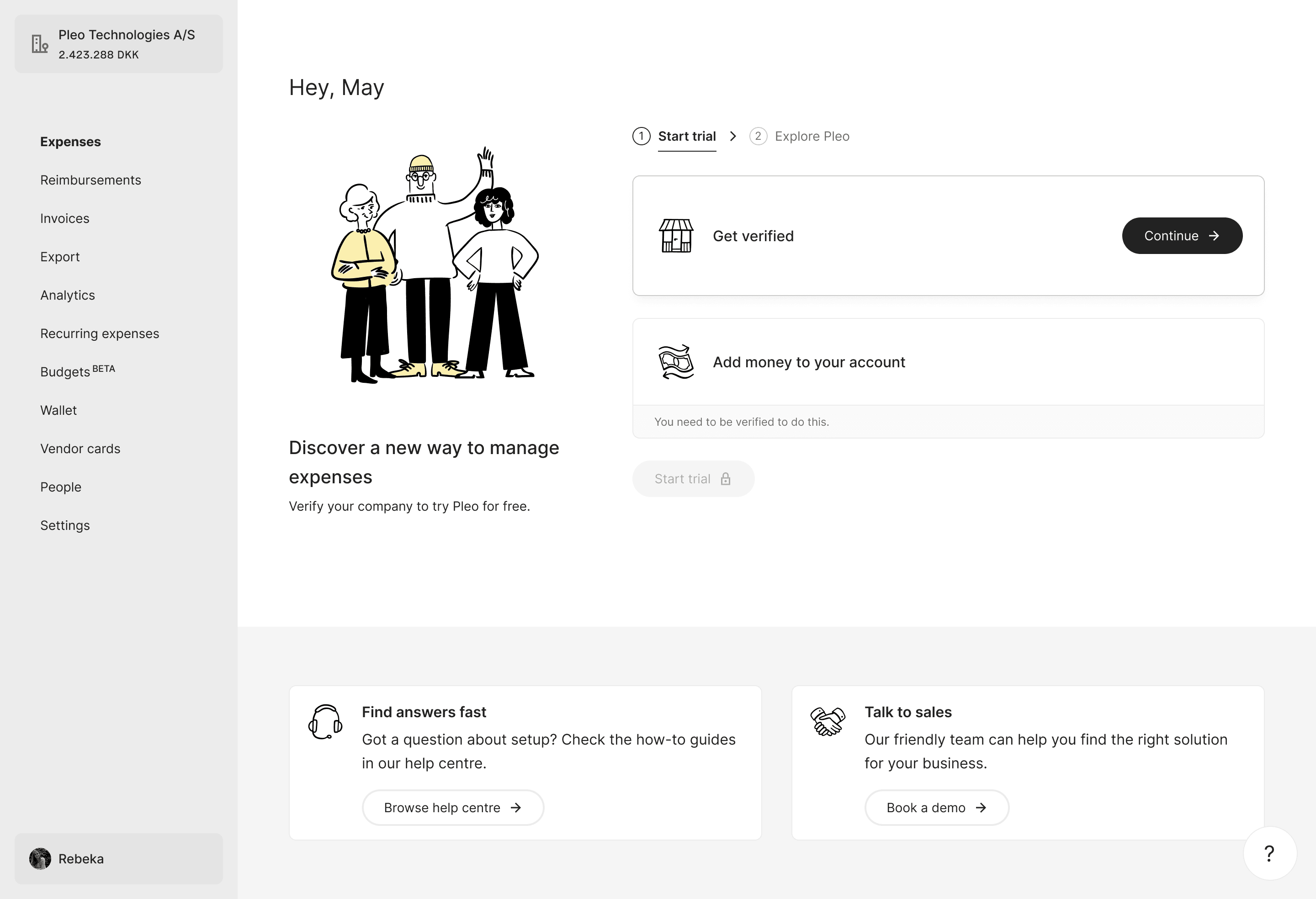

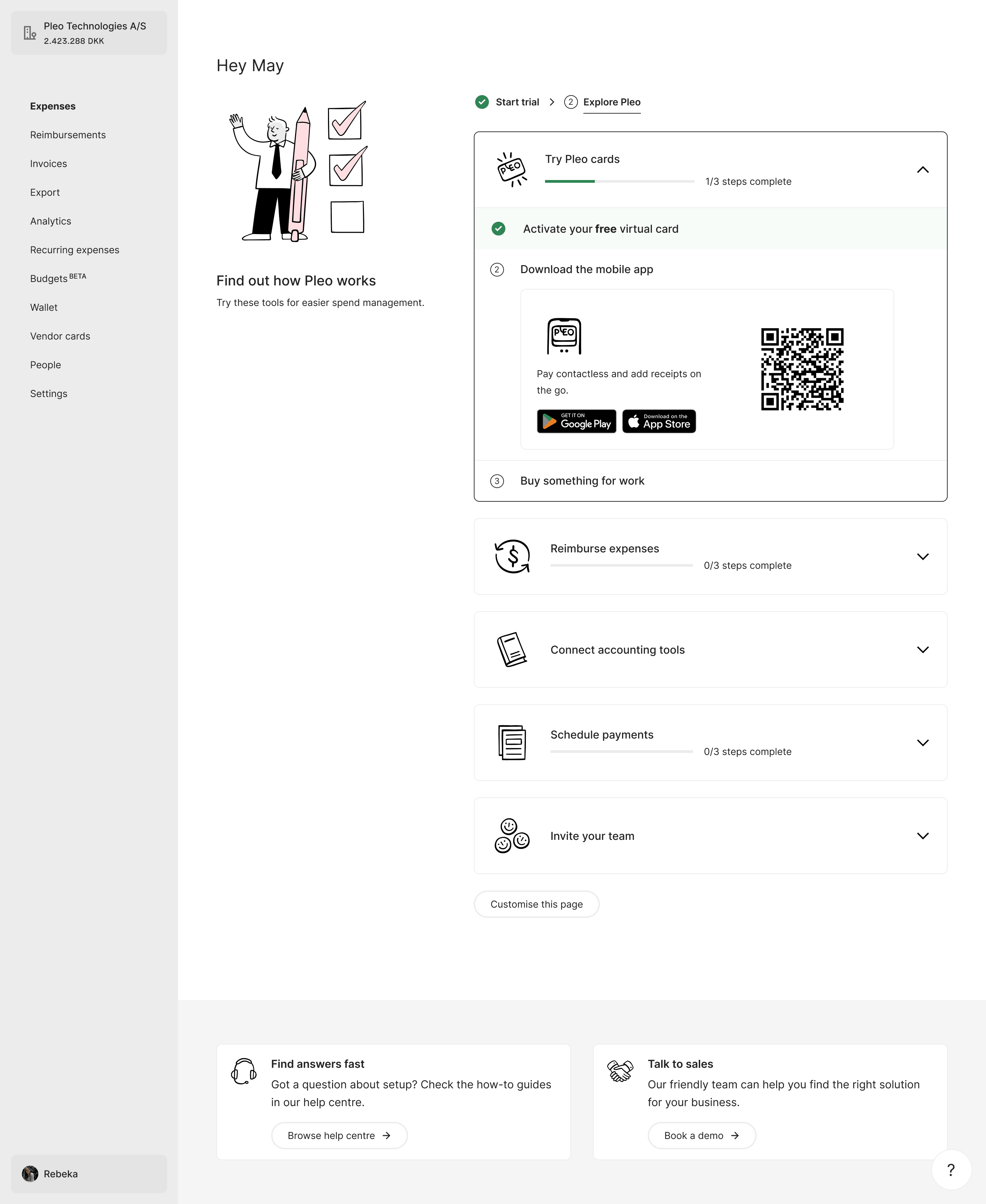

Designing a wallet that never runs dry

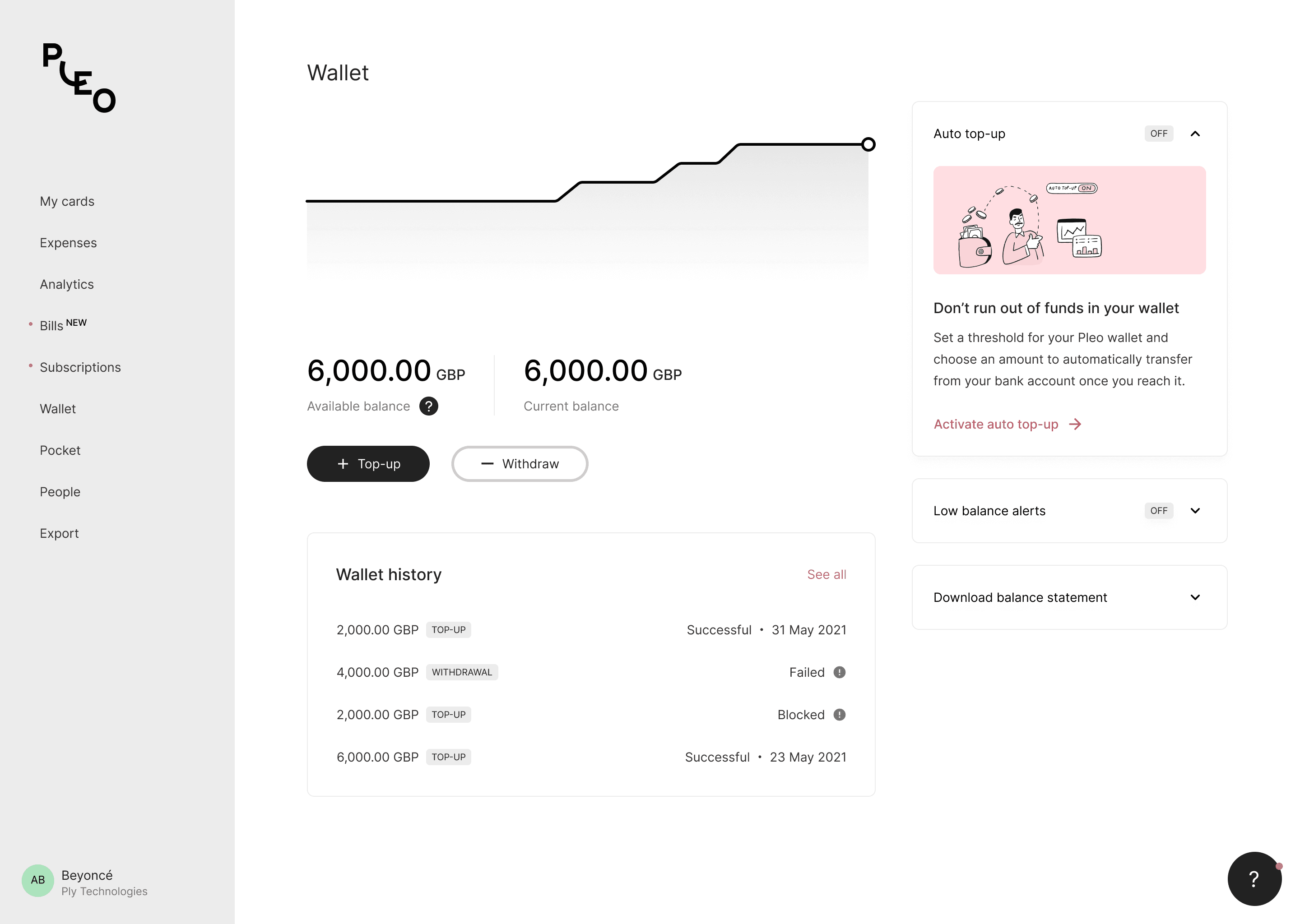

The Pleo wallet is the financial control center for all companies using Pleo to manage spending and expenses. It's typically managed by admins, who are required to add money to it in order to enable spending for invoices, card payments, and subscriptions.

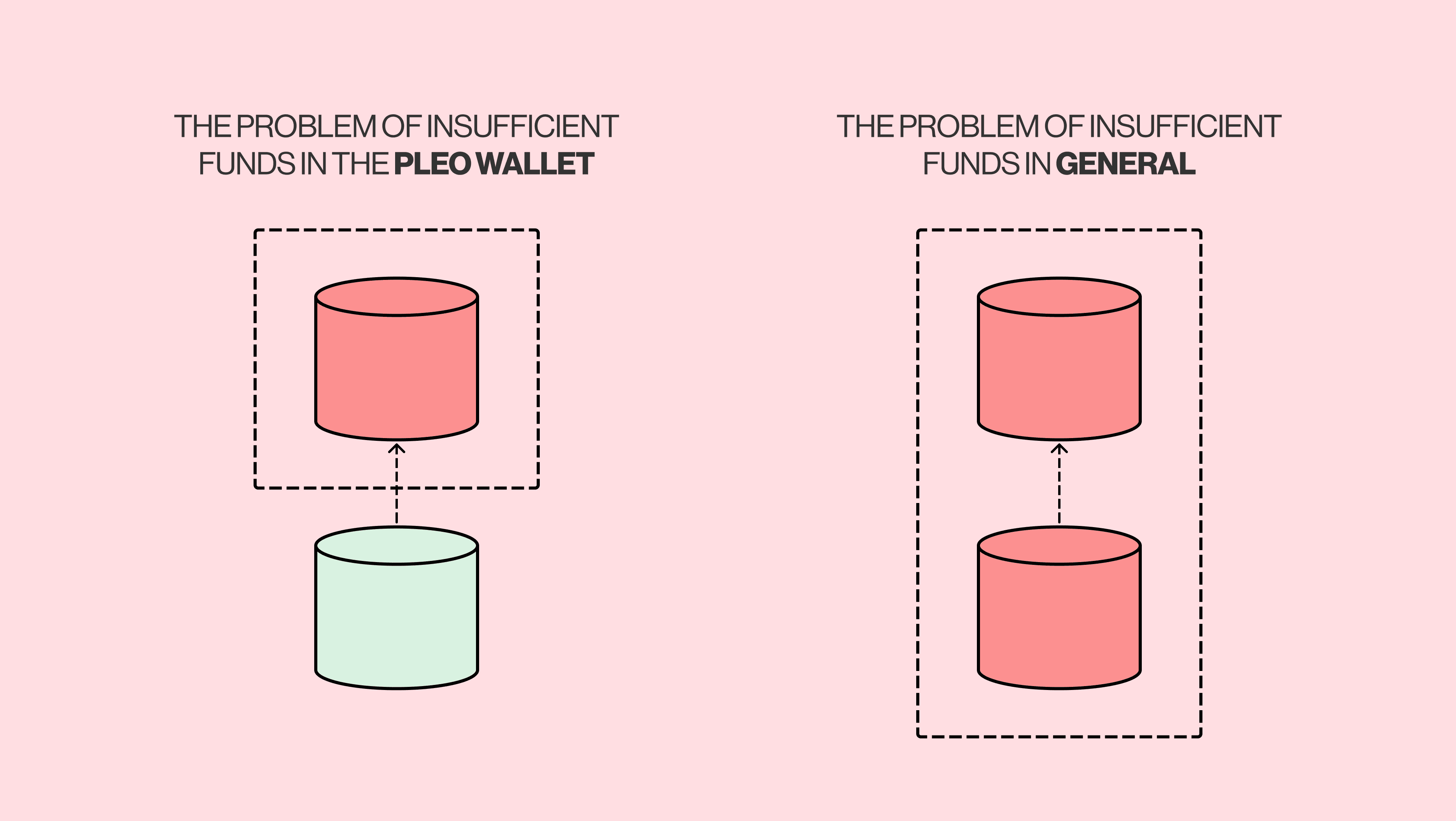

However, keeping that wallet funded at the right level is harder than it sounds, and when it runs dry, spending stops.

More than 50% of all Pleo customers between 2021 and 2022 experienced a transaction decline due to insufficient funds in their Pleo wallet.

Why it's a problem

Pleo makes money when there's a spend from the wallet. If there's a declined spend, there's no revenue, and no profit. A decline is also a moment of friction and embarrassment for the employee standing at the checkout.

How do we solve this?

Three bets, each attacking the problem from a different angle:

- Optimise for speed: make it faster to add money to the wallet, so funding is never the thing that holds spending up.

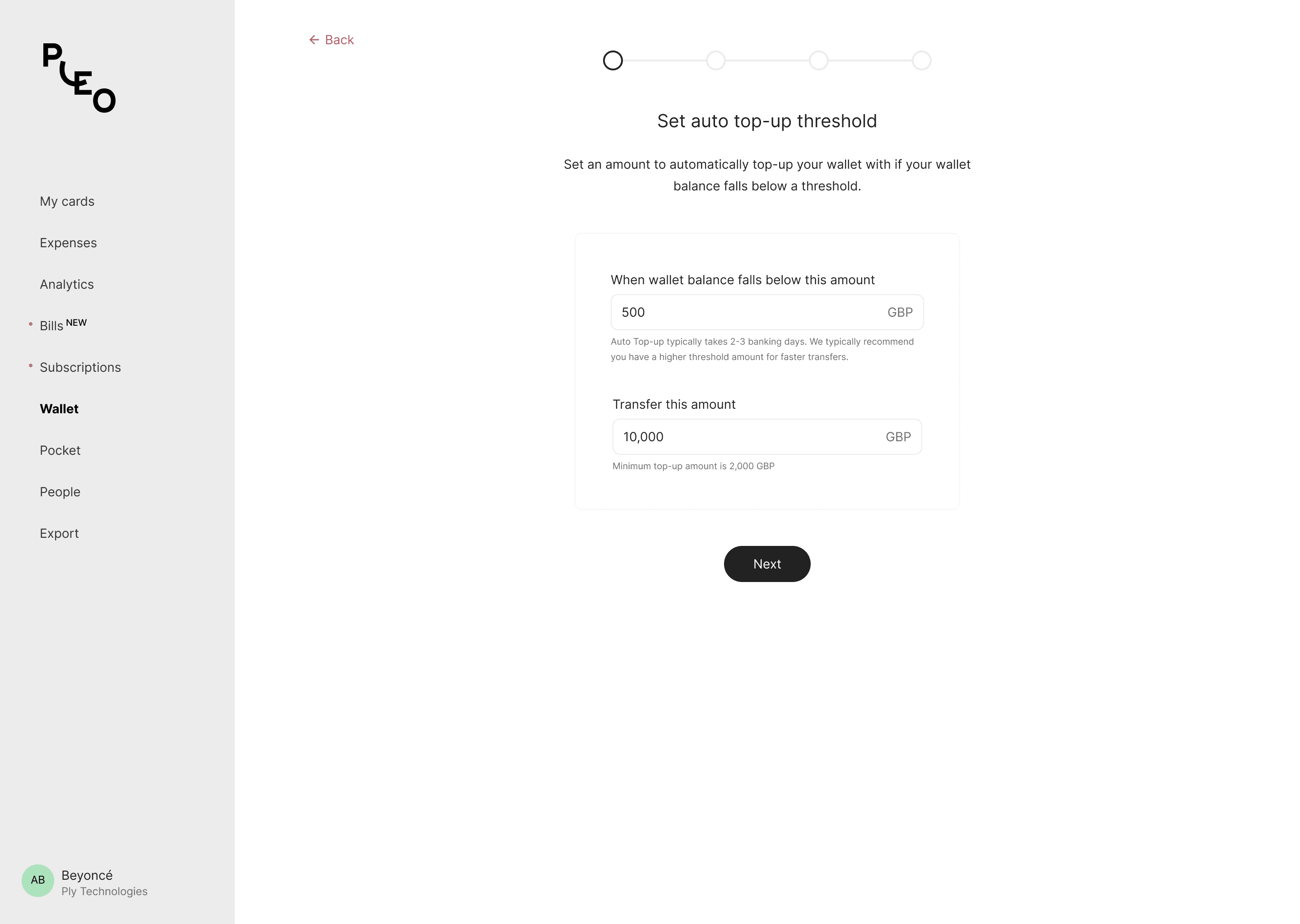

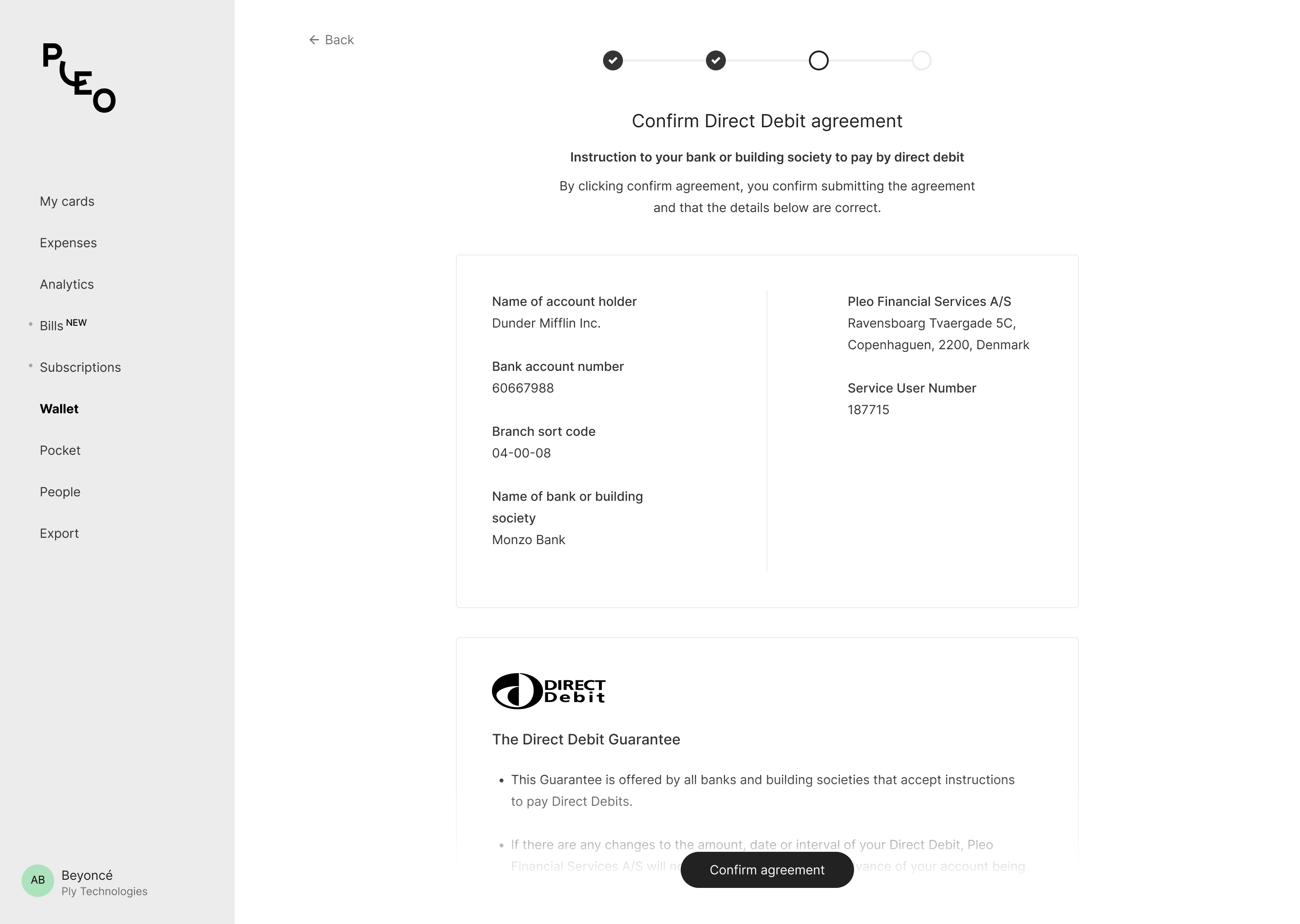

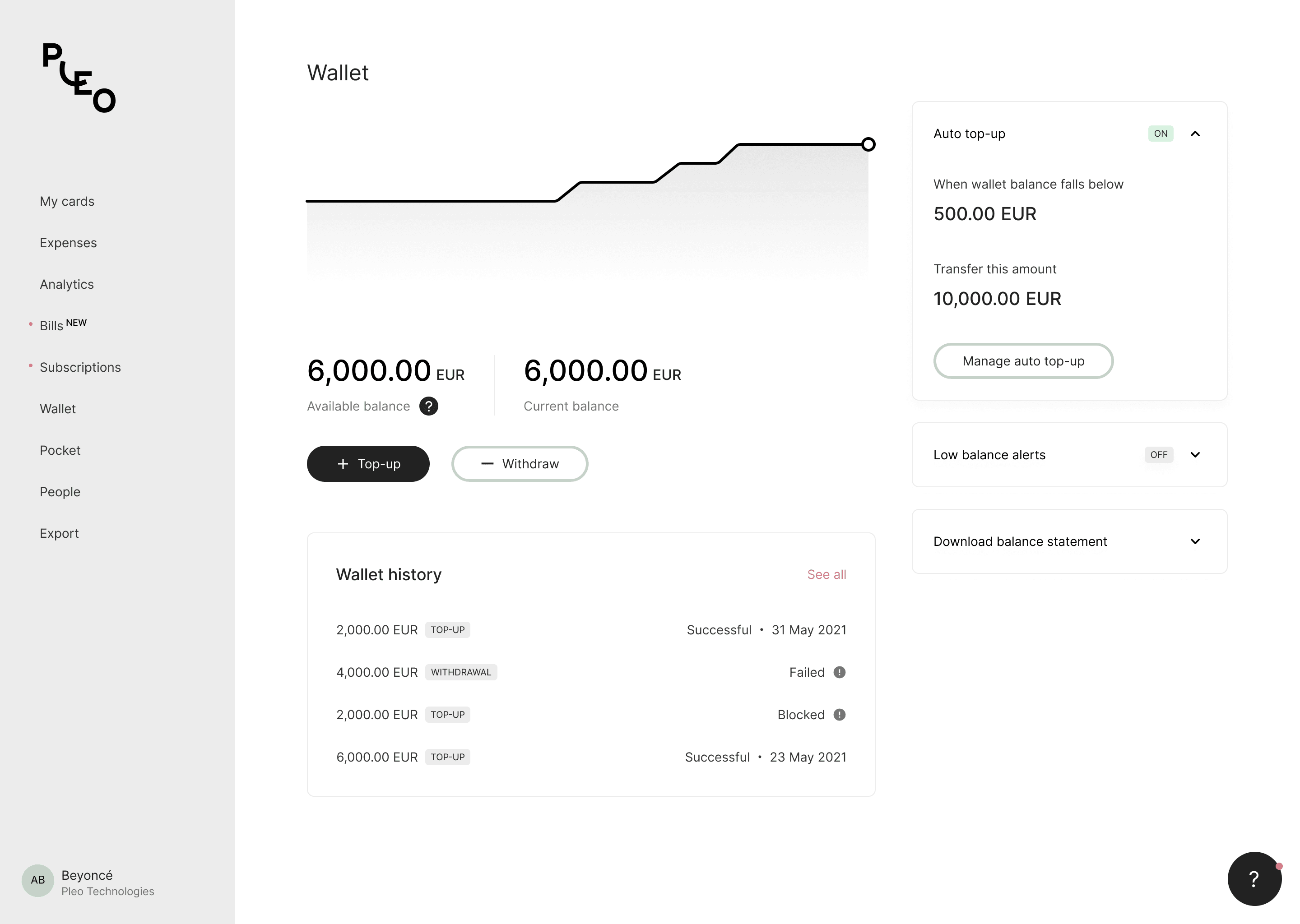

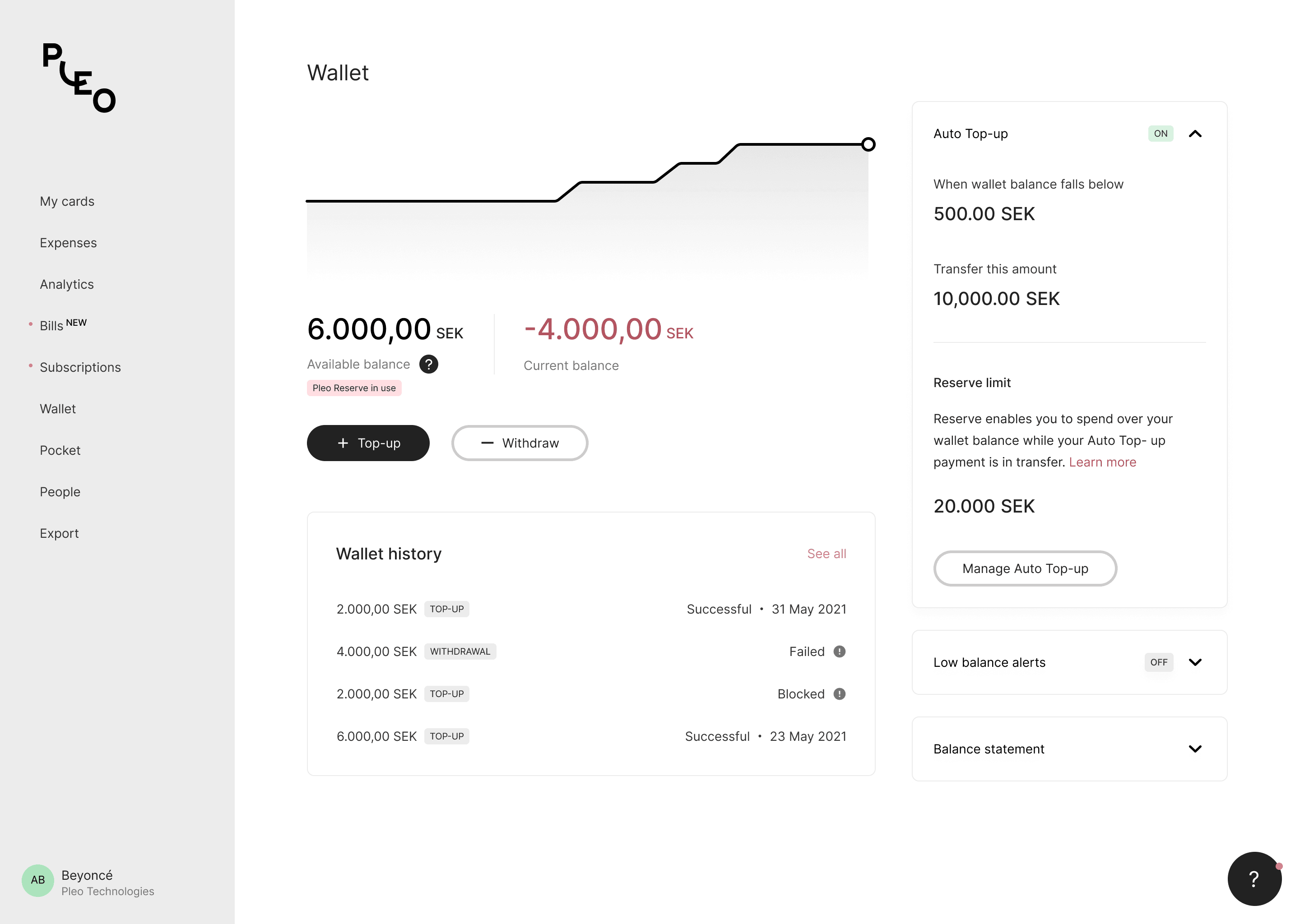

- Automate the wallet: take topping up off the admin's plate entirely, so no one has to think about keeping it funded.

- Introduce credit: flip the model: what if the wallet were credit-first, so spending isn't gated on a balance at all?

The team

1 designer (me), 1 engineering manager, 1 product manager, 1 frontend engineer and 4 backend engineers.

For over 8 months the team didn't have a product manager, so I led that function in collaboration with the engineering manager.

Open Banking in the UK

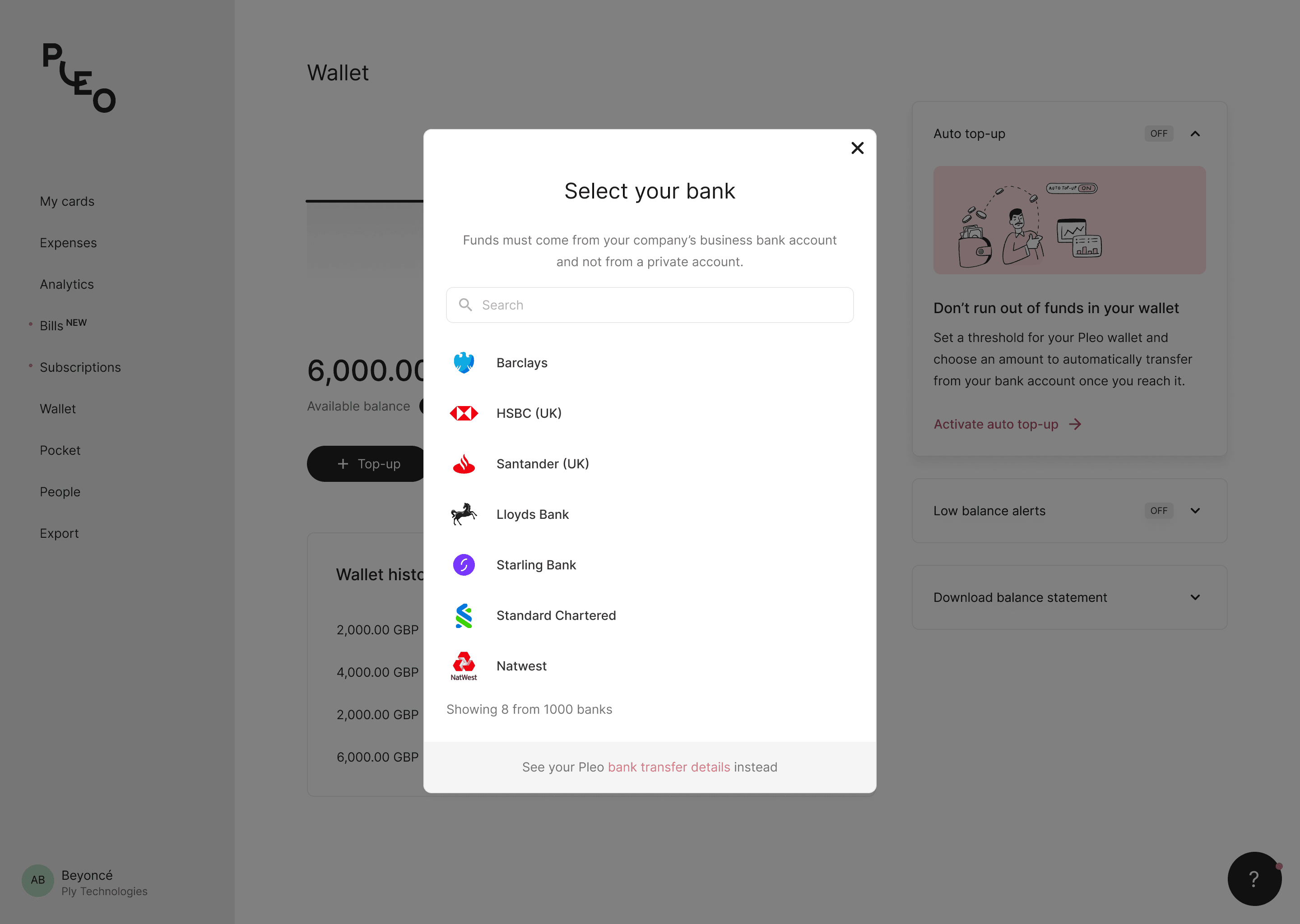

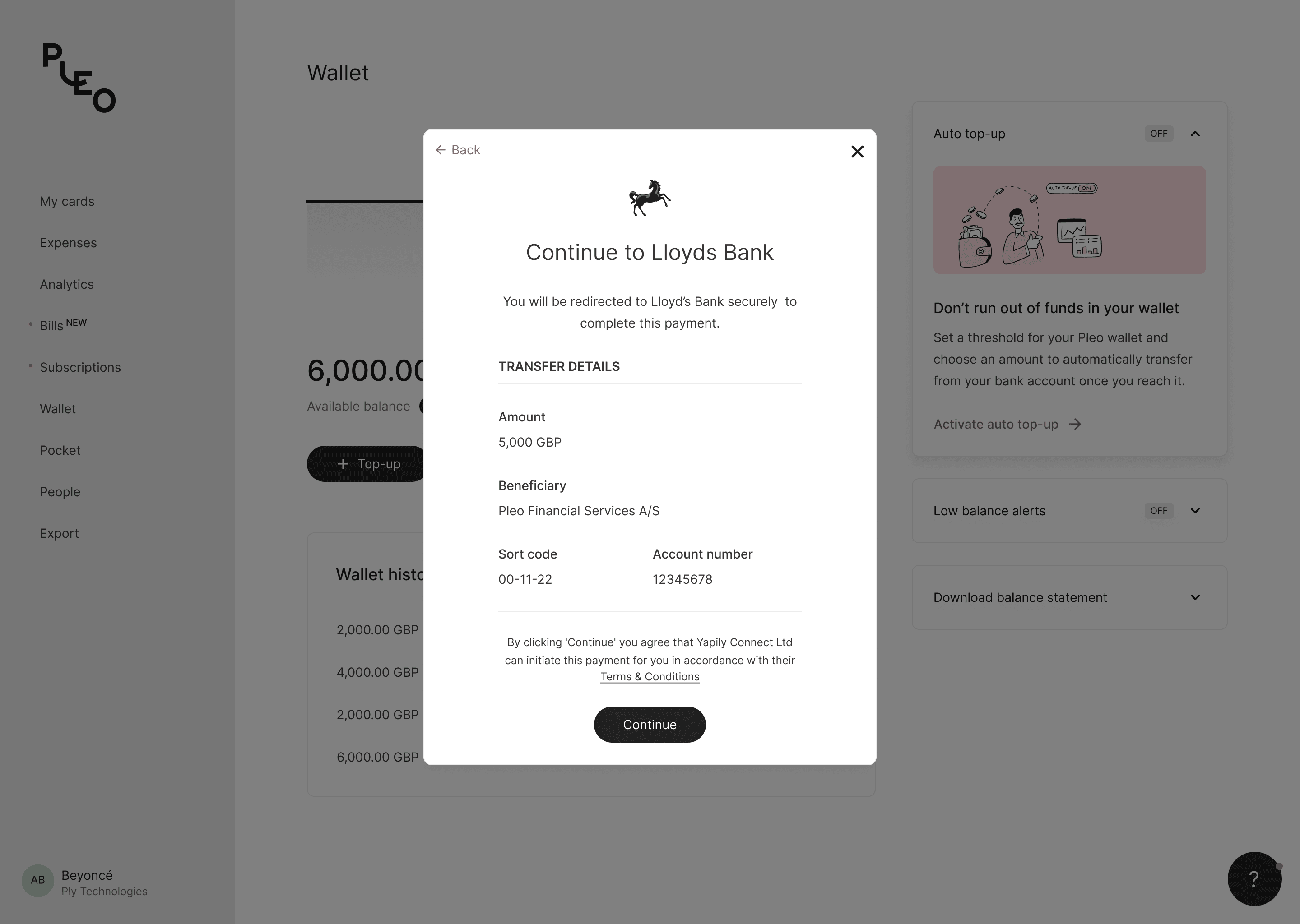

The idea was simple: the faster an admin can move money into the wallet, the less often it runs dry. The biggest lever was the top-up itself.

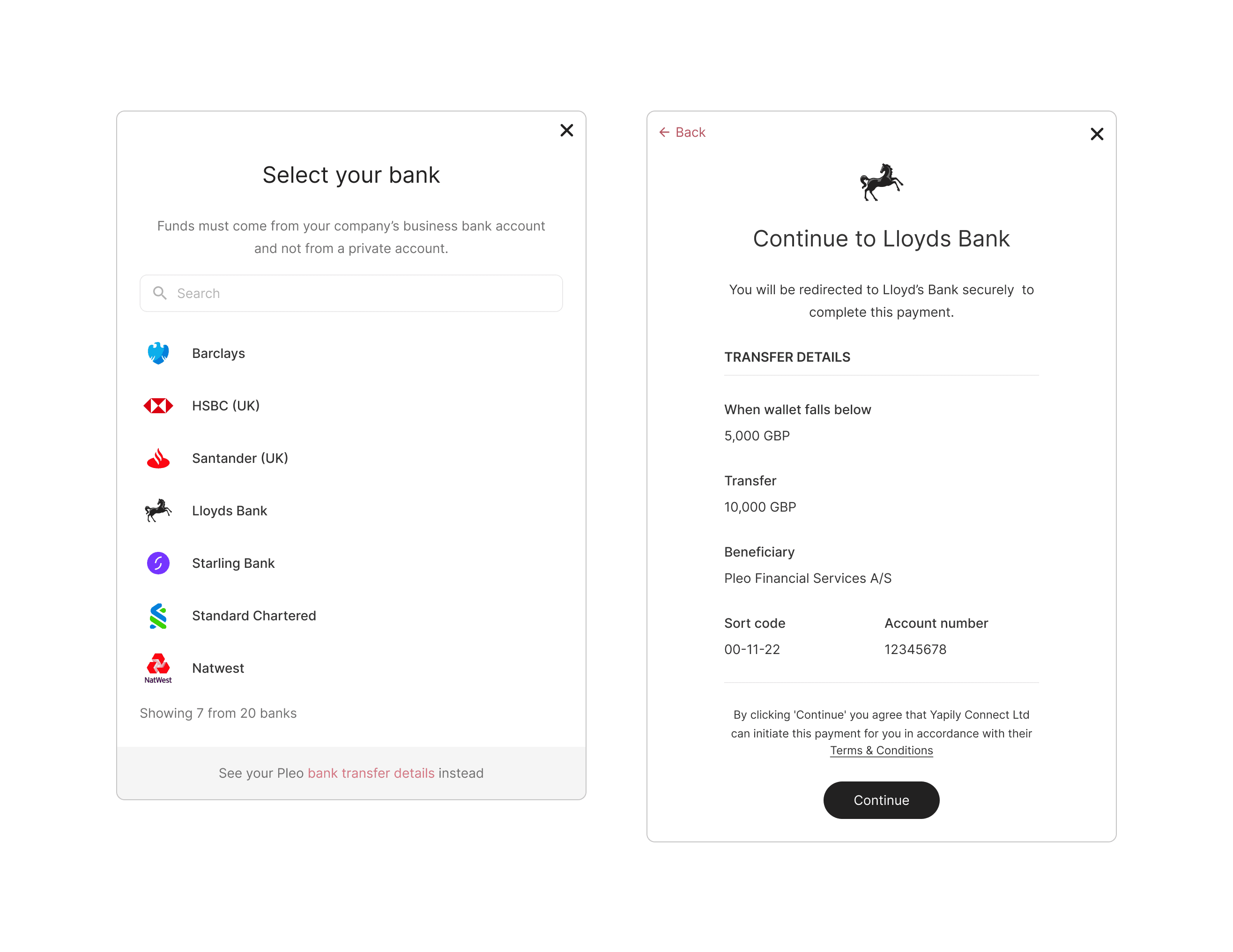

Top-ups had always been manual bank transfers: slow, hard to trace, and clumsy to do, which made a customer's first top-up a poor first impression. So we partnered with Yapily, Europe's largest provider, to build a faster, personalised top-up experience for Pleo's customers across the UK and Europe with Open Banking.

The design process

The work ran as a loop, not a line. It moved from user research through design, testing and build, into a beta rollout and the feedback that fed the next round.

We collaborated closely with Yapily, NatWest and JP Morgan the whole way, validating each flow with real customers before shipping to the first 15% of UK businesses.

Discovery

We started by sitting with admins — the people who actually keep wallets funded — to understand how money moved through their companies and where it got stuck.

The kick-off mapped the funding journey end to end, surfacing the moments where a wallet quietly ran dry without anyone noticing until a card was declined.

For GDPR reasons, I'm not able to show screenshots of UXR transcripts and usability tests.

Design explorations

The first question we asked ourselves: “How might we design a simple experience around a possibly complex process?” Open Banking reaches into a customer's own bank: consent screens, redirects and verification steps that all happen outside Pleo.

We explored ways to keep that machinery out of sight, holding the customer on a single, confident path from deciding to top up to watching the money land, so the complexity underneath never became theirs to manage.

Outcome, impact and challenges

Open Banking quickly became a default way to fund a wallet: faster top-ups, higher retention, and fewer declines.

35% of all top-ups in the UK and 57% in the Netherlands are now Open Banking transactions. Repeat Open Banking customers saw 90% retention and fewer declines than customers who hadn't adopted it.

But two challenges remained:

- An admin always has to remember to make a transfer.

- Open Banking was only available in 2 markets.

Both came down to the same thing: a top-up still depended on someone remembering to make one. The next bet was to take that person out of the loop.